Finance Lecture Series

An Initiative of the Financial Research and Trading Laboratory of IIM Calcutta

The Finance Lab of IIM Calcutta, under the Finance Lecture Series, will organize a talk by Prof. Yakov Amihud of Stern School of Business, New York University (NYU-Stern) on December 29, 2015 at 4 pm. The talk will be held in the Finance Lab. Yakov will speak on “The Pricing of the Illiquidity Factor’s Systematic Risk”.

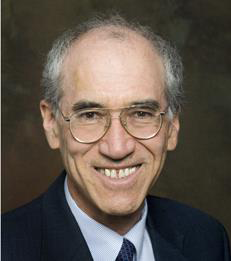

The profile of Prof. Yakov Amihud

Yakov is Ira Leon Rennert Professor of Entrepreneurial Finance at the NYU-Stern. His research includes the evaluation of corporate financial policies, mergers and acquisitions, initial public offerings, objectives of corporate managers, dividend policy, and law and finance. The focus of his research is the effects of liquidity of assets on their returns and values, and the design and evaluation of securities markets' trading methods. On these topics, Amihud has done consulting work for the NYSE, AMEX, CBOE, CBOT, and other securities markets. He has published more than seventy research articles in all top finance journals including, Journal of Finance, Journal of Financial Economics, Journal of Banking and Finance, Review of Financial Studies and also edited/ co-edited five books on topics such as LBOs, bank M&As, international finance, and securities market design. The details of his work may be accessed in http://people.stern.nyu.edu/yamihud/

Yakov is Ira Leon Rennert Professor of Entrepreneurial Finance at the NYU-Stern. His research includes the evaluation of corporate financial policies, mergers and acquisitions, initial public offerings, objectives of corporate managers, dividend policy, and law and finance. The focus of his research is the effects of liquidity of assets on their returns and values, and the design and evaluation of securities markets' trading methods. On these topics, Amihud has done consulting work for the NYSE, AMEX, CBOE, CBOT, and other securities markets. He has published more than seventy research articles in all top finance journals including, Journal of Finance, Journal of Financial Economics, Journal of Banking and Finance, Review of Financial Studies and also edited/ co-edited five books on topics such as LBOs, bank M&As, international finance, and securities market design. The details of his work may be accessed in http://people.stern.nyu.edu/yamihud/

Abstract of His Talk

Yakov presents a liquidity factor IML, the return on illiquid-minus-liquid stock portfolios. The IML, adjusted for the common risk factors, measures the illiquidity premium whose annual alpha is about 4% over the period 1950-2012. Yakov then tests whether the systematic risk (β) of IML is priced in a multi-factor CAPM. The model allows for a conditional β of IML that rises with observable funding illiquidity and adverse market conditions. The conditional IML β is positively and significantly priced, and remains so after controlling for the beta of illiquidity shocks.

The Finance Lab of IIM Calcutta cordially invites you to attend the talk. Please book your seat by sending a confirmatory email to Ms. Priyanka Dasgupta (asstmgr_finlab@iimcal.ac.in). Seats are limited. Registration fee is Rs. 200/- only. Accommodation may be made available on payment basis.