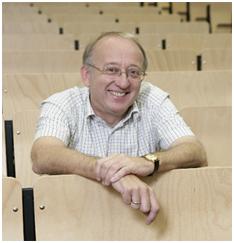

The Finance Lab, under the Finance Lecture Series, will organize a talk by Prof. Paul Embrechts of Swiss Federal Institute of Technology, Zurich on January 17, 2013 at 11:30 am. The talk will be held in the Finance Lab. Paul will speak on “Risk, Regulation and Statistics”.

The profile of Prof. Paul Embrechts

Paul Embrechts is Professor of Mathematics at the ETHZ (Swiss Federal Institute of Technology, Zurich) specialising in actuarial mathematics and quantitative risk management. Previous academic positions include the Universities of Leuven, Limburg and London (Imperial College, and the London School of Economics). Prof. Embrecht is an Elected Fellow of the Institute of Mathematical Statistics, Honorary Fellow of the Institute of Actuaries, Corresponding Member of the Italian Institute of Actuaries, past Editor of the ASTIN Bulletin, on the Advisory Board of Finance and Stochastics and Associate Editor of numerous scientific journals. He is a member of the Board of the Swiss Association of Actuaries and belongs to various national and international research and academic advisory committees.

Abstract of his talk

The talk will start with a review of the so-called Basel regulatory framework in order to explain where statistical methods enter into the calculation of risk capital for the trading book of a bank. Technically, the talk concerns high-quantile tracking of (financial) time series. A review of several methodologies will be given and a new method introduced. The latter is based on a Bayesian approach for regime switching models combined with Extreme Value Theory. Several examples will highlight the results obtained.